ECONOMIC AND FISCAL REGIME OF THE CANARY ISLANDS (REF)

The Canary Islands' economic and tax regime offers significant benefits for investors and businesses operating in the archipelago. This regime, known as Régimen Económico y Fiscal de Canarias (REF), aims to promote economic development, investment attraction and job creation in the region.

One of the main features of the REF is its geographical location. The Canary Islands lie outside the customs territory of the European Union, but are an integral part of the European Economic Area. This means they benefit from a system of reduced or even exempt customs duties for imports and exports, allowing companies to access international markets more competitively.

In addition, the Canary Islands offer a number of tax incentives and benefits for businesses that decide to settle in the archipelago. Some of the main benefits include:

Reduced corporate tax: companies setting up in the Canary Islands can benefit from a reduced corporate tax rate, which is lower than in the rest of Spain and many other European countries.

Reduced Value Added Tax (VAT): the Canary Islands applies a reduced VAT rate, the so-called "IGIC" (Impuesto General Indirecto Canario), which is lower than the standard VAT rate applied in most other European countries.

Exemption from excise taxes: some goods, such as fuels, alcohol, tobacco and soft drinks, are exempt from excise taxes in the Canary Islands, allowing reduced costs for businesses and consumers.

Canary Island Economic Zones (ZECs): businesses that locate in ZECs may be eligible for additional tax benefits, such as full or partial exemption from corporate and labor taxes for certain periods of time.

Research and development (R&D): expenses incurred on R&D are eligible for significant tax breaks, including a 45 percent tax deduction for R&D expenses incurred.

Real estate investment facilities: real estate investors can benefit from tax breaks and facilities in the purchase of real estate, especially for tourism or commercial purposes.

These tax measures and benefits make the Canary Islands an attractive place for domestic and international investors who wish to benefit from a favorable business environment and significant tax incentives. However, it is important to carefully consider the specific regulations and requirements to take advantage of these benefits, as there may be specific conditions and limitations for each measure.

In conclusion, the Canary Islands' economic and tax regime provides a favorable environment for investment and business through a series of tax breaks and competitive advantages. This regime contributes to the economic development of the archipelago and the attraction of new investment, creating opportunities for entrepreneurs and companies interested in establishing themselves in the region.

VAT: ABSENT

ZEC:

Canary Island Special Zone with 4% taxation;

RIC:

Tax Reserve for Investment

DEC:

Deduction for Investment in the Canary Islands

IGIC: 7% on Internal Transactions

THE CANARY ISLANDS

ARE SPANISH ISLANDS LOCATED IN THE SUBTROPICAL ATLANTIC OCEAN PART OF THE EUROPEAN UNION

Spain promotes the economic development of the Canary Islands and, with the full authorization of the European Union, in order to economically compensate for the islands' specific, extremely peripheral island location, reserves for them significant tax breaks applicable to companies wishing to operate in the Canary Islands.

It consists of 7 islands, with 2 million 127 thousand inhabitants covering an area of 7,450 sq. km. and with 15 million tourists a year, present 12 months out of 12, because of the always mild and pleasant climate and excellent quality of life.

ZEC ZONE.

The Canary Special Zone applies territory of all the Canary Islands.

All new enterprises, whether industrial, commercial or service enterprises belonging to the list of permitted activities, can be part of the Zec.

Requirements: tax domicile in one of the Canary Islands;

At least one administrator will have to be a resident of the Canary Islands;

Make a minimum investment of €100,000 (Gran Canaria or Tenerife) or €50,000 in the other Islands in the first two years;

Create at least five or three jobs within the first six months;

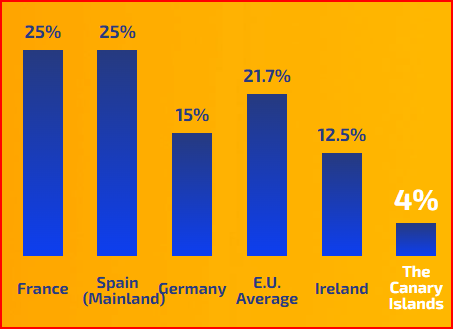

Zec companies enjoy an ageviolated corporate tax rate of 4 percent, and double tax treaties signed by Spain are applicable.

RIC:

Canary Investment Reserve

The Canary Islands Investment Reserve (RIC) is a tax incentive for investment in the Canary Islands that, for businesses, operates on the tax base of the tax.

RIC is a big advantage that allows up to 90 percent of net taxable income to be set aside in an accounting reserve for reinvestment in the Canary Islands.

Therefore no tax is paid on the profits set aside in the RIC reserve.

DEC:

Deductions for Investment in the Canary Islands

The DIC is a decrease in tax and is applied to the tax due resulting from net income, and is therefore a tax deduction.

DIC, is compatible with RIC.

Beneficiaries are companies and legal entities subject to corporate tax domiciled in the Canary Islands or otherwise having a permanent establishment in the Canary Islands.

In addition, the benefit is granted to sole proprietorships and professionals operating in the Canary Islands, subject to the Canary Islands Economic and Tax Regime.

The DIC is a deduction of 25 percent of the amount of quota investments, up to the limit of 50 percent of them, from the corresponding tax, minus the amount of deductions for double taxation and deductions.

IGIC:

Taxes on domestic transactions in the Canary Islands (similar to Vat) of 7%.

No VAT is applied in the Canary Islands. In fact, a similar tax applies, which is the IGIC (Impuesto General Indirecto Canario), but only on transactions within the Canary Islands.

The IGIC tax is an Indirect Tax similar to VAT that currently has a rate of 7% for "ordinary" goods and services and go up to a maximum of 15% for "non-primary" goods and services (car purchase or rental, purchase of precious goods, etc., etc.) or luxury goods and services; in some particular applications it is reduced to ZERO (purchase of new technologies, information technology , etc., etc.).

Thus, it is an indirect tax levied on goods and the provision of services.

It applies to both entrepreneurs and professionals who conduct their business in the Canary Islands within the 12-mile territorial sea limit.

In some cases, the IGIC tax rate is zero. Therefore, living or setting upa business in the Canary Islands, is extremely advantageous.

Bonus for the Production of Material and Consumer Goods in the Canary Islands

Bonus for the Production of Material and Consumer Goods in the Canary Islands.

This is a tax incentive that reduces the corporate tax rate and, if applicable, the IRPEF income tax rate.

The purpose of this tax instrument is to encourage establishment and increase productive activities throughout the archipelago.

This incentive represents a 50 percent reduction in taxes on income from the sale through export of physical goods produced in the Canary Islands.

This tool is compatible with other tax incentives under the REF Canary Islands Economic and Fiscal Regime.

The legal framework of the European Union is in force in the Canary Islands with the highest guarantee of legal security

The Canary Islands are fully integrated into the EU, so all European laws and regulations are applicable in the Islands.

As an outermost region, the Canary Islands enjoy a number of economic and fiscal incentives fully approved by the European Commission.

The EU legal system has one of the highest standards of international legal certainty, which means greater protection for companies based in the Canary Islands in many aspects, including data protection, free competition and financial regulations.

ORDINARY TAXATION OF PROFITS PRODUCED BY MERCHANT COMPANIES

ORDINARY TAXATION OF CORPORATE PROFITS

For new companies, the reduced rate of 15 percent applies

The reduced rate of 15% is applicable to the first 2 years in which the company earns income.

The rate rises to 20 percent on incomes over 300,000 euros.

From the third year on, the ordinary rate, which is 25 percent, applies.

REF Economic and Fiscal Regime of the Canary Islands

The Canary Islands Archipelago has been treated uniquely both administratively and economically and fiscally since the 16th century after its incorporation into the Crown of Castile, due to its insular status and geographic distance from Europe, as well as its scarcity of natural resources, enjoying, for all that, a special tax regime based on freedom of trade in imports and exports, the non-application of monopolies and customs and consumption tax exemptions, as well as the existence of local taxes.This regime incorporates in its content the principles and rules applicable as a result of the recognition of the Canary Islands as an outermost region of the European Union (Article 349 of the Treaty on the Functioning of the European Union), with the objective that Canarian citizens have equal opportunities before the group of citizens of the European Union, having to modulate state action in economic policies to this end.Considering that it is an outermost region of the European Union, the economic and fiscal regime of the Canary Islands includes a series of economic measures aimed at promoting the economic, social and territorial cohesion of the archipelago and the competitiveness of its strategic sectors, all in order to ensure a situation in which the average cost of economic activity in the Canary Islands allows the island economy to compete with that of the rest of the national territory.The measures currently envisaged by the Law refer to the following areas: transportation and telecommunications; energy and water; trade promotion; tourism promotion and rehabilitation; regional economic incentives; job creation and promotion of social integration; investment incentives; Vocal training; promotion of culture...,in recent years, other branches of economic activity have become relevant, such as waste management or renewable energy development, among others.Main aids under the Taxation Act:- RIC - Reserve for investment in the Canary Islands.

- DEC - Deduction for investments in West African territories and for propaganda and advertising expenses.

- Investment deductions.

- Deductions for investments in film productions, audiovisual series and live performances of performing arts and music made in the Canary Islands.

- Investment incentives.

- Bonus production.

- General indirect tax of the Canary Islands.

- ZEC - Canary Islands Special Zone.

- Canary Islands Free Zones.