Canary Islands Special Area

WHAT IS THE CANARY ISLANDS SPECIAL ZONE Z.E.C. (Canary Islands Special Zone)?

The Canary Islands Special Zone (ZEC) is a low-tax zone created under the Canary Islands Economic and Fiscal Regime (REF), with the aim of promoting the economic and social development of the Archipelago and diversifying its productive structure.

The ZEC is extended to the entire territory of the Canary Islands, so there are no limitations of restricted areas for settlement.

The ZEC was authorized by the European Commission (EC) in January 2000 and is regulated by Law 19/94 of July 6, 1994.

WHO CAN STAY IN THE ZEC (Canary Islands Special Zone)?

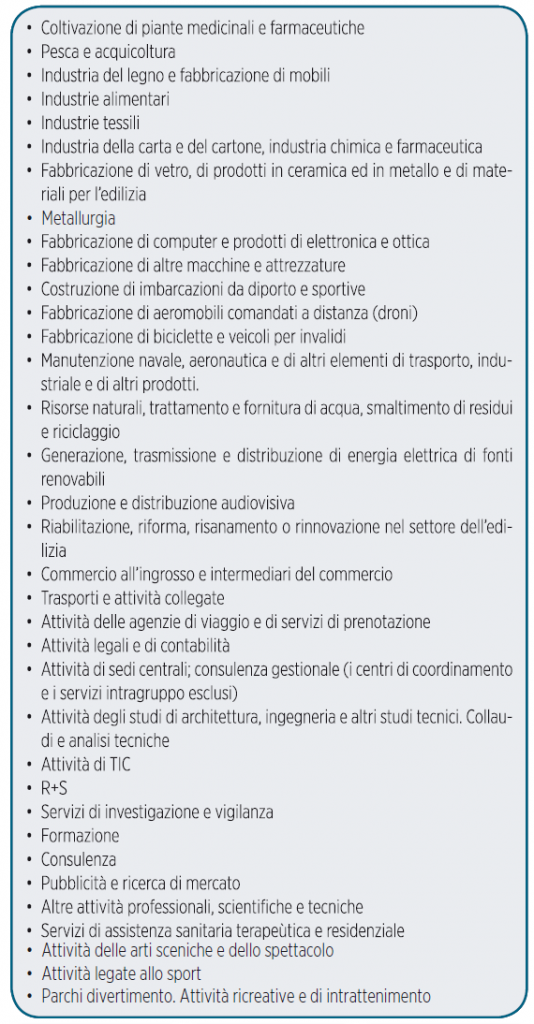

- All companies, entities and branches that intend to carry out an industrial, commercial or service activity;

- That fall under the list of permitted activities;

- Who submit a project approved by the public body formed by the ZEC Consortium.

- That make a minimum investment of € 100,000 (in the case of the islands of Tenerife and Gran Canaria) or € 50,000 (in the case of La Gomera, El Hierro, La Palma, Fuerteventura or Lanzarote) in fixed assets related to the business, within the first 2 years after registration.

- Create at least 5 or 3 jobs, depending on whether or not they are located in the capital islands, within 6 months

TAX ADVANTAGES OF ZEC ENTITIES

CORPORATE TAX

ZEC entities will be subject to Spain 's current corporate tax at a reduced rate of 4 percent.

This reduced rate will be applied above certain tax base limits based on job creation and capital stock.

The minIm needed is a share capital of 50,000 and creation of 3 jobs

EXEMPTION FROM INCOME TAX FOR NON-RESIDENTS

Dividends distributed by subsidiaries of ZEC Entities to their parents residing in another country, as well as interest and other income earned from the sale of equity to third parties and capital gains from movable assets obtained without the intermediary of a permanent establishment will be exempt from withholding tax.

This exemption applies to income earned by residents in any state when such income is paid by a ZEC entity and is derived from transactions materially and actually carried out in the geographical area of the ZEC.

However, these exemptions do not apply when the income is obtained through countries or territories with which there is no effective exchange of tax information or when the parent company has its tax residence in one of those countries or territories.

TRANSFER TAX AND STAMP DUTY

ZEC Entities will be exempt from taxation for this tax in the following cases:

The acquisition of goods and rights intended for the development of the ZEC Entity's activity in the geographical scope of the ZEC.

Corporate operations carried out by ZEC Entities, unless they are dissolved.

The documented legal acts related to the transactions carried out by these entities in the geographical area of the ZEC.

IGIC EXEMPTION.

(GENERAL INDIRECT TAX OF THE CANARY ISLANDS)

In the ZEC ( Canary Islands Special Zone) regime , deliveries of goods and supplies of services made by ZEC Entities to each other, as well as imports of goods made by them, will be exempt from taxation by the IGIC.

BORDER ZONES.

Possibility to set up in Free Zones with with particolaru economic advantages, especially economic advantages for the practice of import and export and the improvement of goods there.

COMPATIBILITY WITH OTHER TAX INCENTIVES IN THE REF.

(Economic and Fiscal Regime of the Canary Islands)

Within the limits of EU rules on cumulation of aid and under certain conditions, ZEC tax benefits are compatible with other REF tax incentives such as:

- RIC (Reserve for Investment ) Deduction from taxable income of up to 90% of net retained earnings set aside in special accounting reserve;

- Investment Deduction;

- Reclamation for the production of physical goods by 50%;

- Deductions for investments in strategic sectors highest in all of Spain;

- Various exemptions in indirect taxation;

MAXIMUM GUARANTEE IN LEGAL SECURITY

Integrated into the legal and judicial system of the European Union (EU), the Canary Islands offer full security and protection to individuals and businesses.

Results of tr

WHAT REQUIREMENTS ARE NEEDED TO BE A ZEC ENTITY?

REQUIREMENTS

To be a newly incorporated company, entity or branch with domicile and effective place of management in the geographical area of the ZEC which is made up of the entire territory of the Canary Islands, without any limitation of location and therefore a company can set up wherever it wants as long as it is in one of the Canary Islands.

At least one of the directors must reside in the Canary Islands.

Make a minimum investment of €100,000 (for the islands of Tenerife and Gran Canaria) or €50,000 (in the case of La Gomera, El Hierro, La Palma, Fuerteventura, or Lanzarote) in business-related fixed assets within the first 2 years of registration.

- enterprises that create at least 5 or 3 jobs, depending on whether or not they are located in the capital islands, within the 6 months after registration and maintain this average in the years it is annexed to the ZEC.

- That its corporate purpose falls within the permitted activities within the scope of the ZEC.

- That an explanatory project of business development with the impact on employment be submitted and the project be approved by the ZEC Public Consortium;

EXEMPTION FROM MINIMUM INVESTMENT REQUIREMENTS

The following enterprises are eligible to apply for the investment waiver, provided that employment exceeds the required minimum:

- innovative enterprises,

- enterprises operating in priority sectors

(audiovisual, video games and technology); - Human resource-intensive enterprises;

AUTHORIZATION PROCESS

The company submits an application for prior authorization to the Rector Council of the Consortium for registration in the Official Registry of ZEC Entities, enclosing a descriptive project of the economic activities to be carried out with expected spin-offs in employment and economic development with the required documentation attached.

Within a maximum of two months, the Consortium decides on the matter and in case of a positive outcome, the company or entity will be able to register in the Official Register of ZEC Entities and start operating under the advantageous regime.